Q and A

The stock market’s meteoric rise since March 30 is raising questions from clients. Let’s start with the most asked question:

Q. Since the Iran conflict started, oil prices are higher along with higher inflation and interest rates. How can the market rally when these factors point to potential trouble ahead?

A. We are stuck between a closed Strait and an AI boom. It is abundantly clear which one of those is winning at the moment, as markets continue to notch new all-time highs on the back of a stunning AI and tech-fueled run in equity markets.

Over the longer-term, earnings drive stock prices. It is as simple as that. You could even say that profits are the lifeblood of our capitalistic system. Growing corporate earnings have provided fuel for this entire bull market.

The growth in corporate earnings we are seeing now is extraordinary. On March 31 coming into the Q1 earnings season the expected growth for S&P 500 profits was 13.1% year-over-year – an excellent number. Actual earnings growth will come in at about 27% (this is not a typo). This is incredible. Earnings growth for calendar 2026 is expected to be 20.6% (all earnings figures are from FactSet). You could say earnings from the AI boom are responsible for the latest mega-rally in stock prices.

Other positive factors aiding the rally include unexpected jobs growth in non-farm payrolls the last two months surpassing forecasts by a wide margin. And GDP growth is fine – neither reaccelerating nor collapsing. Is this “ho-hum” economy good enough for markets to continue pushing higher? We think so (with caveats described in the answer to the next question).

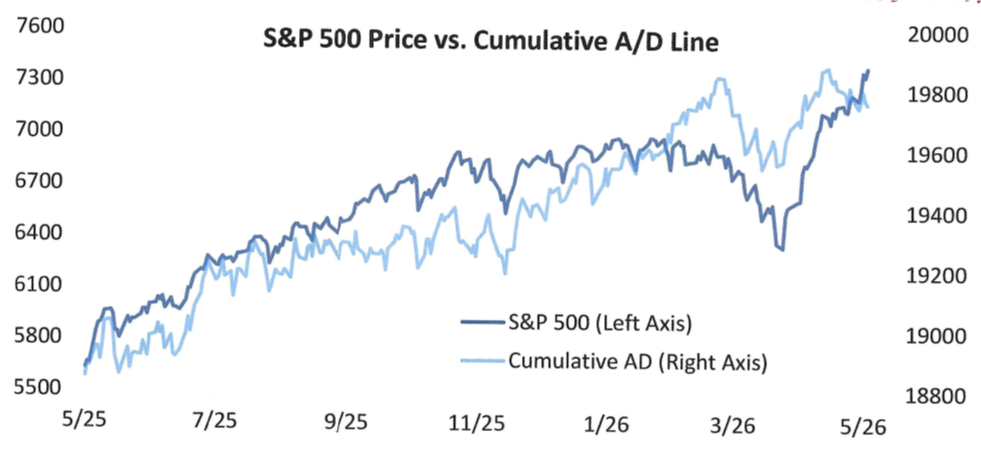

Q. Has the recent stock market rally been solid or does it look like a potential bubble?

A. The most recent rally in stocks has not been as broad as we would like. The bulk of the market’s move to new highs has been driven by a small number of stocks in Tech, including semis. Bulls argue that the rest of the index will eventually catch up.

The S&P 500’s cumulative advance/decline line remains well below prior highs as the index surged to new records last week. See the graph below. Notice the spike higher in S&P 500 prices along with a declining A/D line:

Source: Bespoke Investment Group

Another technical breadth indicator, moving averages, also looks sketchy. If you were to look at the percentage of stocks trading above their 50- and 200-day moving averages, it would be hard to tell the market has set records. This is not to say these breadth measures can’t catch up with prices, but for now we think breadth needs to improve for the market to have another leg up from here.

Are we in a bubble? After all, semiconductor stocks rose 38% in April. Are investors getting giddy with stock gains?

Spotting a bubble is harder than it seems. If investors could identify a bubble, it probably wouldn’t form in the first place. Investors would see it begin to form and promptly step aside or bet against it. Over-pricing in parts of the market does not constitute a bubble.

One historical sign of a bubble is a tidal wave of stocks issuance like the late 1990s or even 2020-2021 (SPACs). So far at least, new stock offerings haven’t flooded the market.

Another sign of a bubble is performance chasing behavior. Momentum investing dominates. However, we are seeing contrarian, not performance chasing, behavior. A bubble is buy the rip, not buy the dip.

In our humble opinion on bubbles, we are not in one.

Q. A number of respected Wall Street economists are expecting a U.S. recession by the end of this year. Could this happen?

A. Anything is possible but we don’t see it.

Bears on the economy point to …

- Housing market stagnation which has represented a drag on GDP growth for seven of the past eight quarters. Housing is a big part of our economy.

- The possibility of a weaker jobs market. Low-hire low-fire won’t last.

- Higher inflation combined with lower economic growth resulting in stagflation or worse.

- A tighter Fed or at least one where cuts later this year are off the table. Our view is that raising interest rates would act like a ‘tax’ on consumers on top of the higher oil price ‘tax.’ We don’t expect this to happen. But will the Fed cut rates any time soon? Not likely in our view.