EARNINGS DRIVE STOCKS, NOT HEADLINES

The drawdown in stocks has been accelerating since our last commentary. Through yesterday the S&P 500 is down 7.3% YTD and Nasdaq 10.5%. The average stock in the S&P 500 is down over 20% since the market peak late last year. War has been the catalyst for the March decline but it is important to remember the primary catalyst for stock prices over the long term is earnings. After all, the war will eventually end and investors will then focus again on market fundamentals including earnings. We are pleased to see that S&P 500 earnings estimates are going up for 2026 and are now expected to rise 17% this year – up from a 15% forecast for growth at the beginning of the year (source: FactSet). The earnings backdrop is currently a solid tailwind for stocks.

The combination of lower share prices and higher earnings estimates are driving valuations considerably lower. For example, the S&P 500 was trading at 23x forward earnings last fall compared to 19x forward today. The tech sector’s forward P/E has dropped from 30+ to 20, the same valuation it was at in 2019. Valuations are no longer rich.

Other key positives include:

- AI is not going away. The AI boom turned “bubbly” in 2025 but has had a much needed rest after the huge rally we saw last year.

- Both initial and continuing jobless claims, good measures of employment, are not suggestive of any significant weakness in the job market.

- AI’s impact on productivity is likely positive. Strong per worker output growth creates an incentive to hire more workers. Generally speaking, periods of high productivity subsequently lead to strong hiring. This is contrary to the narrative about AI job losses.

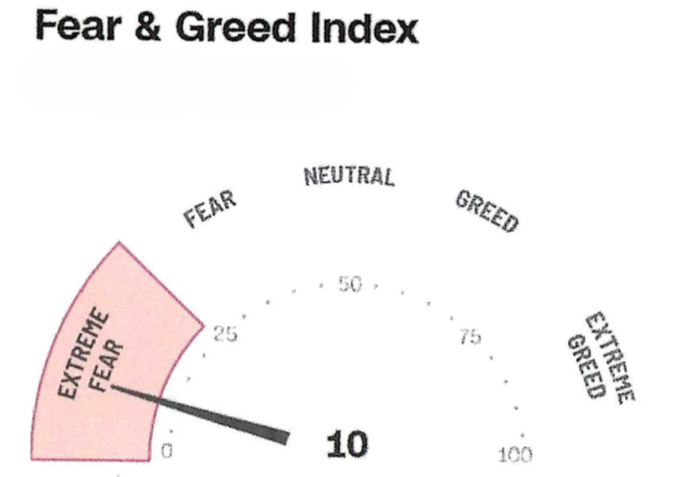

- Investor sentiment, a contrarian indicator, was bullish at the end of 2025 but the bears have since come out of hibernation. For example, CNN’s Fear and Greed Index has fallen into “Extreme Fear,” a potentially bullish signal. See below:

Source: CNN

- The S&P 500 is currently in extreme oversold territory and upside mean reversion will occur at some point.

We have to also acknowledge there is plenty going wrong right now in both the equity and fixed income markets. Here are a few lowlights:

- Market technicals are decidedly bearish. We have seen nothing but lower highs and lower lows since the war began. We will need to see higher highs and higher lows again for the technical backdrop to turn more bullish.

- The mega-caps continue to trade terribly. We are going on six plus months of deteriorating technicals. Until they can turn things around, it is going to be hard for the broader market to turn higher.

- Inflation was already above-target before tariffs pressured it higher. And now we have a fresh price shock from the energy markets due to the war in Iran. How will the Fed react?

The Fed’s March 18th policy statement left descriptions of the economy mostly unchanged and the war’s effects as uncertain. The Fed was willing to look through energy prices as long as they did not raise long-term inflation expectations. But for how long? The markets are not as sanguine as the Fed appears to be. Investors are now pricing in a roughly one-in-three chance of a rate hike by year-end thanks to the inflation war has created. This compares to the market expectation of 2-3 cuts this year back in December. Higher policy rates would remove one of the pillars of this bull market. We think the probability of the Fed raising rates is low but is nevertheless a risk.

- Death by AI is still a fear. Certain companies and industries are expected to be hurt by AI.

——————————-

What should an informed long-term investor do armed with all the market information available today? After all, things could get worse before they get better.

Above all else, stay invested!

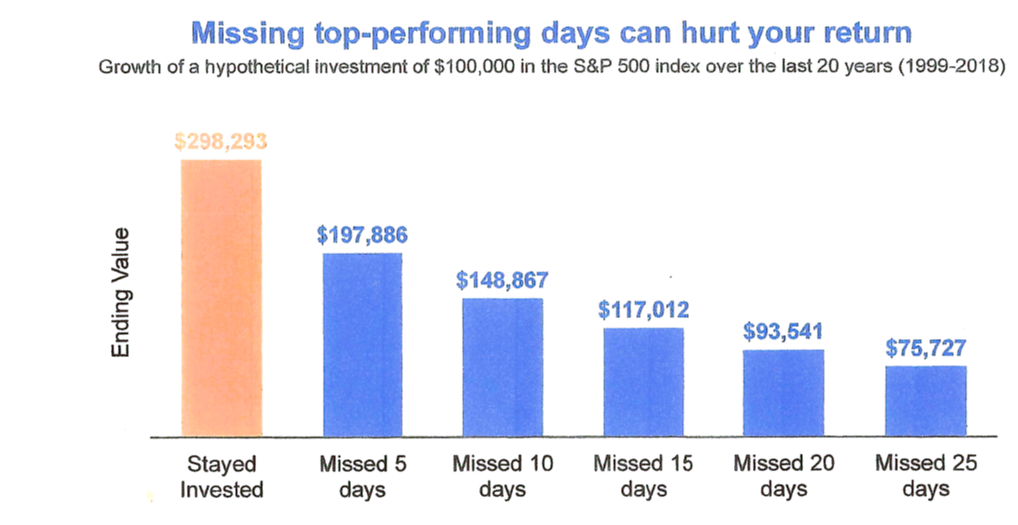

Below are the results of a study showing how investors can’t afford to miss the market’s best days (which often follow the market’s worst days). The study shows actual market performance over a 20-year period ending in 2018.

Sources: Blackrock, Bloomberg

If you stayed fully invested over this time period, your $100,000 initial investment grew to $296,293. But if you missed just the five best days (over 20 years), your account value would be only $197,866, or 33% less than the fully invested investor. Missing more of the best days only compounds the problem by punishing the market-timer even more. The lesson here is a strong one: market timing doesn’t work.