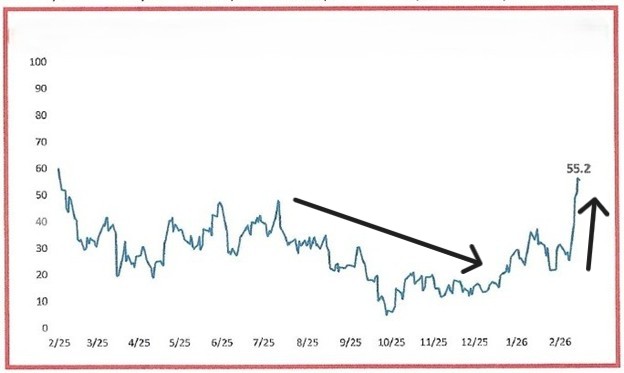

In January we wrote the “three-headed monster” (courtesy of Bespoke Investment Group) was flashing green. The three variables – oil, Treasury yields, and the dollar – were all in downtrends which bodes well for stocks. In the last three weeks we have seen a massive reversal. All three variables are now moving higher including a spike in oil following the U.S. attack on Iran. Making matters worse, the potentially inflationary implications of higher oil prices have also pushed Treasury yields higher and the dollar has rallied on a flight to safety trade.

Below is a graph of the average level of the three variables combined over the last year. Notice the recent spike:

3-Headed Monsters Average Level Relative to 52-Wk Range (%): Last 12 Months

Source: Bespoke Investment Group

This model is telling us we have serious market headwinds while we are at war. No surprise. The trend may have to change before we can expect a firmer stock market.

OIL PRICES UP. STOCKS DOWN.

Oil up. Stocks down. It has been that simple. The war in the Middle East has made energy prices the market’s sole focus, crowding out earnings, interest rates, economic data, AI or issues in private credit. If oil falls on signs the Strait of Hormuz supply constraints are easing, we expect a rally in stocks. If oil prices continue to climb, it signals a continuation of the bottleneck. If that is the case, the economic consequences will be difficult to contain regardless of how insulated the U.S. economy is versus most of its global peers.

The main question is how long the Iran conflict lasts. The question is not just academic. Core inflation came in hotter than expected last week and higher oil prices will likely jack up future headline numbers. That complicates matters for the Fed, which might like to lower interest rates to boost a cooling job market, but its hands might be tied. Already the expectation of the next rate cut has been pushed out to the second half of the year.

Last week Q4 GDP growth was revised down from 1.4% to 0.7%. With such meager growth does this mean higher oil may tip us into a recession. After all, two of the four recessions since the late 1980s followed spikes in crude oil. Not so fast. GDP growth in Q4 was negatively affected by the government shutdown taking away 116 basis points (1.16%) of growth. Excluding the federal government shutdown, growth would have been closer to 2%. Government spending should be a tailwind this quarter even with the current partial shutdown. And AI also remains a significant tailwind but, as usual, consumption is the key driver of U.S. growth.

Also, U.S. consumers are much less exposed to oil prices than they have been in the past. For example, personal consumption expenditures on vehicle fuel are under 2% of total outlays, compared to 3.5% in the early 2010s. In other words, the risks of higher oil prices are lower for consumer spending that has historically been the case.

Don’t let the narrow trading range of the S&P 500 fool you into thinking it has been a quiet year for stocks. There has been massive dispersion. The S&P 500 may be within 5% of its 52-week high, but more than 100 stocks are up or down at least 20%. Eight of the eleven sectors are experiencing larger drawdowns than the index. Breadth is awful. Dull market? Anything but.

There has been no panic in the equity markets or the fixed income markets, a good sign. Maybe just a minor price re-setting. That is not to say things can’t get worse. The war is at a critical juncture with the Strait of Hormuz closed. Can we re-open the Strait without using ground troops? That possibility is making investors nervous. The war, however, won’t go on forever. And when it ends, the stock market could resume its winning ways off a base of lower share prices – or at least return to more typical fundamental concerns. We will sit tight during this uncertain period. It is never a good idea to trade based on headlines.